A “sexy casino,” where real-estate speculation has moved online.

Polymarket rose to prominence in 2024 by letting users bet on the U.S. presidential election, with trading volume hitting record highs on the night of Trump’s victory.

In November 2025, it signed a partnership with the UFC and entered sports betting. Then, on January 5, 2026, it announced a new experiment:

Betting on home prices.

Polymarket had previously offered markets tied to mortgage rates, but those were essentially derivatives on Federal Reserve policy. This time is different. The new markets allow users to directly bet on whether a specific city’s home price index will rise or fall.

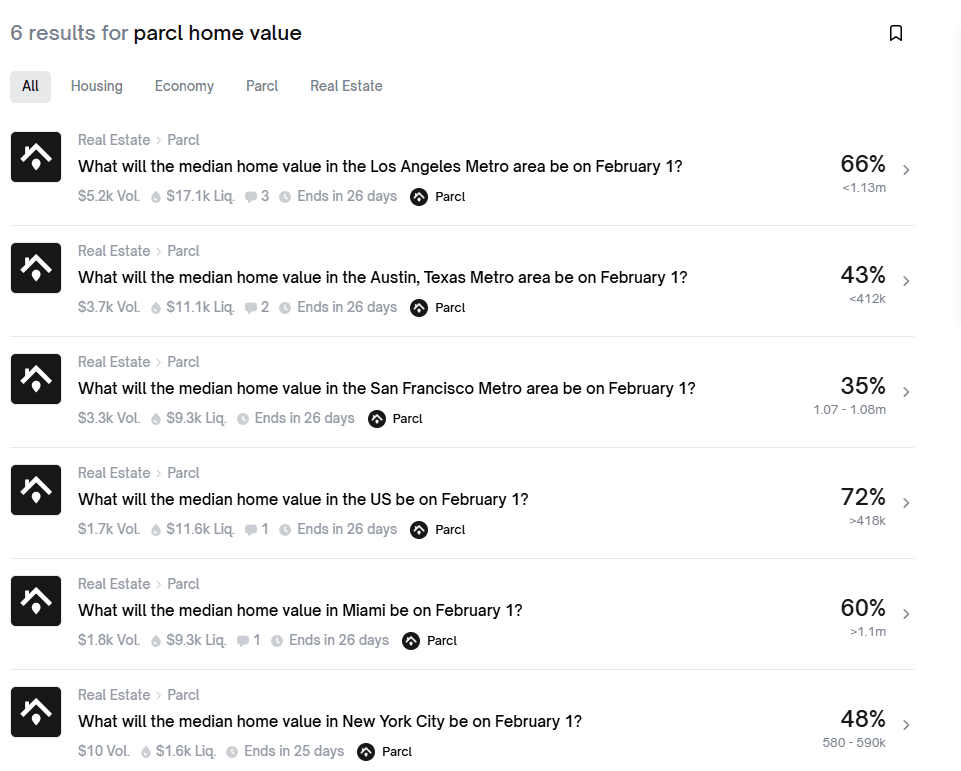

The partner is Parcl, a real-estate data protocol on Solana. The mechanics are simple: choose a city and predict whether its home price index will go up or down next month.

The initial markets include Austin, San Francisco, Miami, New York, plus a national U.S. index.

No down payment.

No mortgage application.

No dealing with agents.

Bet USD 100. Get it right and double your money. Get it wrong and it goes to zero.

Polymarket’s CMO argues that real estate is the world’s largest asset class—worth USD 400 trillion—and therefore deserves to be a “first-class citizen” in prediction markets.

A USD 400 trillion casino, with the entry ticket now reduced to:

The price of a cup of coffee.

This is not entirely new.

Back in 2008, the UK betting exchange Betfair already offered markets on a housing crash. What happened that year needs no retelling. Wall Street was trading CDS, MBS, and CDOs—acronyms few ordinary people understood, but everyone ended up paying for them.

Polymarket has simply translated the same idea into plain language:

Will Miami home prices rise or fall before February 1? Pick one.

According to the partnership announcement, settlement data is provided by Parcl and updated daily—faster than traditional housing indices. Each market comes with a dedicated settlement page detailing final values, historical trends, and calculation methodology.

Transparent. Public. Verifiable on-chain.

It sounds appealing. But current market data tells a quieter story. Even the most liquid market barely has USD 17,000 in liquidity. New York’s market sits at around USD 1,600, and after two days online, total trading volume there was just USD 10.

People are enthusiastic about betting on presidents. Betting on housing prices? It seems most haven’t figured out how to play yet.

For now, this looks less like a mass market—and more like an early adopter playground. Or, put differently:

A hunting ground for whales.

Parcl raised two funding rounds in 2022, with investors including Dragonfly, Coinbase Ventures, and Solana Ventures, totaling over USD 11 million.

Its earlier products were far more aggressive: long and short positions on housing indices, up to 10x leverage, perpetual contracts.

Yes—real estate trading with leverage.

After partnering with Polymarket, the design became more restrained. No leverage. No perpetuals. Just simple binary options: up or down, settle at expiry.

Polymarket itself has been expanding rapidly. Valued at USD 1.2 billion in 2024, by the end of 2025 the parent company of the NYSE, ICE, announced plans to invest USD 2 billion, pushing its valuation close to USD 9 billion.

From betting on presidents, to boxing, to home prices—the catalog keeps expanding. What’s next is unclear. Divorce rates? Birth rates? How long the bubble tea shop downstairs can survive?

As long as there is a data source, anything can become a market.

On-chain analytics have already shown that nearly 70% of Polymarket users lose money, with profits concentrated in a very small number of wallets.

That ratio looks familiar—to crypto trading, and to stock trading as well.

The difference is this: election outcomes are discrete and definitive. You win or you lose. Housing data is not. It comes with lags, noise, seasonality, and methodological disputes. You may think you are making a judgment, but in reality you are betting against statistical definitions.

The traditional logic of buying a home is straightforward: 30% down, a 30-year mortgage, monthly payments that may exceed your salary—but at least the house is yours.

The Polymarket version of “buying a home” is different: bet USD 100, wait a month, double it or lose everything. The house is never yours. It never was.

Which one looks more like gambling?

The last wave of financialized real estate ended with the subprime crisis in 2008. This time, retail traders are allowed at the table.

What progress.

You may also like

Champion's Final Bow: FC Barcelona vs Real Betis – Celebrate the Title with a Home Finale

Best Oil Trading Platform for Crypto Users in 2026

5 Futures Trading Strategies Smart Traders Use to Cut Crypto Fees and Boost Futures Returns

What Is TradFi? How Crypto Traders Can Now Access Crude Oil, Gold, and Global Markets

How WEEX Bridges Crypto and Football: A Deep Look at the LALIGA Partnership Inside the WEEX App

WEEX is not just a LALIGA sponsor. It’s a true partner. From iPhone Dynamic Island to LALIGA-themed app icons and smart posters, see how WEEX brings football passion into every trade — and builds a real bridge between crypto and sports.

FC Barcelona vs Real Madrid Preview: El Clásico – Can Barça Clinch the Title at Spotify Camp Nou?

FC Barcelona vs Real Madrid El Clásico match preview for May 11, 2026. Barça need just 1 point to win LALIGA. Can Madrid delay the trophy? Full preview inside.

At the Stripe conference, I saw the future of the AI economy

Miners welcome a new life

Seven Important Judgments by Claude Code's Founder at the Sequoia Conference

The payment moment of AI agents: Who will become the Stripe of the machine economy?

Morning Report | MoonPay acquires Solana's execution layer DFlow; Strategy releases Q1 financial report; Manta Network announces the termination of Manta staking program

Rented Tracks: What is this wave of stablecoin FX hot money really paying for?

Dialogue Velocity Eric: What is the stablecoin track that the CFO really wants?

Strategy should have said that selling coins is not ruled out

How MegaETH Achieved a TVL of 700m Within a Week of TGE? Analyzing the Packaging Strategy

Futures Trading Hours: Trade Cryptocurrency 24/7 and Earn Back Up to 45% in Trading Fees

Learn futures trading hours and the best time to trade crypto futures. Discover 24/7 market insights, peak trading sessions, and how to earn back up to 45% in fees.

Why is a16z Crypto raising another $2.2 billion to heavily invest in Web3?

Polymarket Underlying Algorithm Explained

Champion's Final Bow: FC Barcelona vs Real Betis – Celebrate the Title with a Home Finale

Best Oil Trading Platform for Crypto Users in 2026

5 Futures Trading Strategies Smart Traders Use to Cut Crypto Fees and Boost Futures Returns

What Is TradFi? How Crypto Traders Can Now Access Crude Oil, Gold, and Global Markets

How WEEX Bridges Crypto and Football: A Deep Look at the LALIGA Partnership Inside the WEEX App

WEEX is not just a LALIGA sponsor. It’s a true partner. From iPhone Dynamic Island to LALIGA-themed app icons and smart posters, see how WEEX brings football passion into every trade — and builds a real bridge between crypto and sports.

FC Barcelona vs Real Madrid Preview: El Clásico – Can Barça Clinch the Title at Spotify Camp Nou?

FC Barcelona vs Real Madrid El Clásico match preview for May 11, 2026. Barça need just 1 point to win LALIGA. Can Madrid delay the trophy? Full preview inside.